FetchLogic Weekly AI Intelligence Report

Week of May 19, 2026

Executive Summary

Funding: The AI startup ecosystem is bifurcating sharply. As of April 2026, 1,730 unicorn startups exist globally, with 887 in the United States, according to BestBrokers’ unicorn valuation tracker. Deal flow data from Mean CEO’s May 2026 analysis reveals capital is consolidating around infrastructure (inference optimization, safety layers) and vertical SaaS (small business workflows). Seed and Series A funding remains robust; late-stage rounds are selective and driven by unit economics rather than growth-at-any-cost narratives.

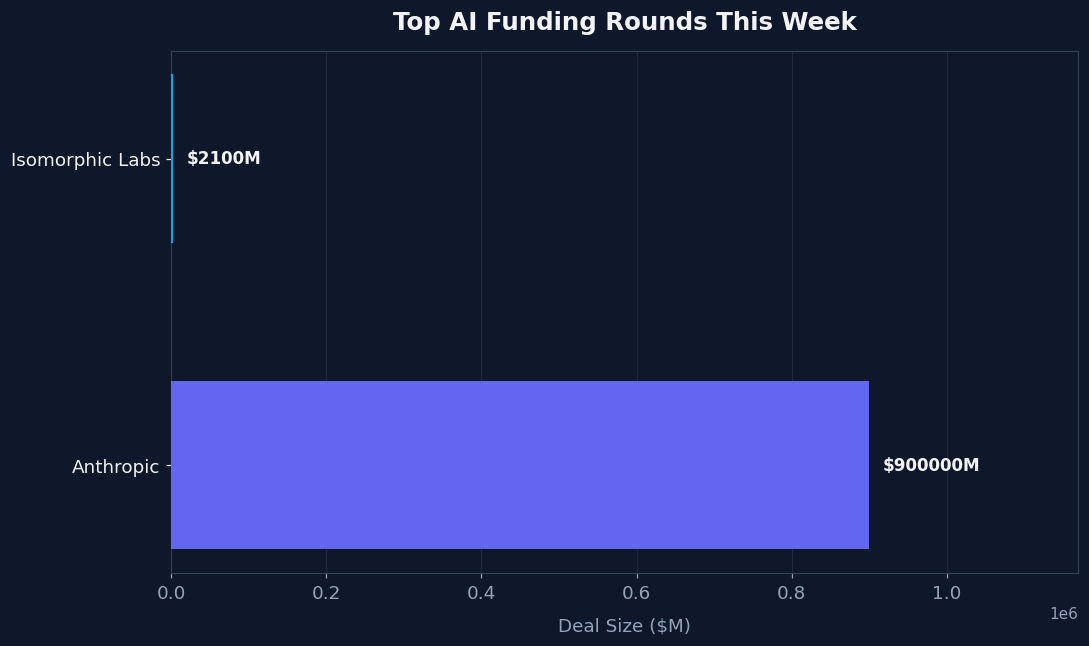

Models & Products: OpenAI and Anthropic are shipping at scale. OpenAI deployed GPT-5.5 Instant as the default ChatGPT model, while Anthropic released Claude for Small Business with 15 agentic workflows and reported 80x year-over-year ARR growth with $44B+ annualized revenue. The capability gap between frontier labs and competitors has narrowed for commodity reasoning; differentiation is shifting to cost-per-inference, reliability layers, and domain-specific tuning. Isomorphic Labs (DeepMind spinout) raised $2.1B for drug discovery, signaling investor conviction in vertical AI applications beyond language.

Policy & Talent: Regulatory fragmentation is accelerating. Colorado’s AI Act, California’s complex compliance regime, and Texas’s TRAIGA framework are now active, per VerifyWise’s May 2026 regulatory overview. Meanwhile, 55% of employers report regretting AI-driven layoffs, a signal that organizational readiness lags capability deployment. Rehiring patterns suggest a bifurcation of labor: senior roles shifting offshore at lower cost, while entry-level AI engineering roles remain scarce.

Funding & Deal Activity

Capital deployment in AI is entering a maturation phase. According to Qubit Capital’s 2026 fundraising trends analysis, the median Series A check size has stabilized at $8-12M while Series B rounds are expanding to $25-40M, a departure from the indiscriminate mega-rounds of 2024-2025. The top 50 AI-funded startups tracker shows that 38% of recent rounds target inference infrastructure or safety systems, compared to 16% in early 2025. This reflects both a real bottleneck (GPU allocation is becoming genuinely scarce) and investor discipline: companies with clear unit economics and wedges into existing workflows are winning allocation.

Anthropic’s fundraising round, on track for a $900B valuation by end of May 2026, is the clearest signal that frontier lab equity is being treated as venture-scale rather than later-stage buyout. This valuation reflects not current revenue ($44B ARR) but embedded conviction that multi-modal agentic systems and enterprise penetration will command 10-15x revenue multiples within 24 months. By comparison, European AI startups face a 35-40% funding discount relative to US peers on identical metrics, a gap widening as EU AI Act compliance costs compound. Geographic arbitrage has become real.

Market Share & Valuations

The private market is consolidating. Of 1,730 global unicorns, 887 are US-based, per BestBrokers’ April 2026 unicorn data. AI and vertical SaaS represent 31% of this cohort by count and 56% by aggregate valuation—a clear overweight. The median unicorn valuation (inclusive of all sectors) has drifted down to $1.4-1.6B from $2.1B in Q4 2025, a 25% contraction driven by both multiple compression and reduced late-stage appetite. However, the top quartile of AI companies—those with $100M+ ARR and gross margins above 70%—is trading at 12-18x forward ARR, a premium that persists despite broader market volatility.

Valuation momentum is now driven by land-and-expand metrics (net retention rate, logo retention) rather than headcount growth. Companies reporting >130% net revenue retention are seeing 40-60% valuation increases in their latest rounds, while those below 110% face 20-30% haircuts or stalled fundraising. This shift reflects institutional investors’ learned experience: AI deployment is moving from experimentation budgets into core workflows, but ROI measurement remains weak. Founders still cannot articulate a clear playbook for upsell beyond “add more seats.”

Big Tech: Product Launches & CapEx

OpenAI and Anthropic are in a sustained sprint. GPT-5.5 Instant became the default model in ChatGPT, a move designed to reduce inference costs while preserving reasoning capability. Meanwhile, Anthropic’s Claude for Small Business release includes 15 pre-built agentic workflows, a direct challenge to OpenAI’s enterprise API strategy. Both companies are targeting the SME market (10-500 employees), where penetration is still <10%, as a beachhead for recurring revenue. PwC's deployment of Claude across hundreds of thousands of professionals signals that enterprise buy-in for non-OpenAI models has crossed a threshold.

CapEx commitments remain elevated but disciplined. Anthropic’s $900B valuation round implies $40-60B in committed infrastructure spend over 24 months; OpenAI’s reported hardware roadmap suggests a similar magnitude. Neither company is publicly disclosing margins, but industry consensus places frontier labs’ inference margins at 45-55% at scale (>$100M monthly revenue), compared to 25-35% for smaller providers. This moat—driven by proprietary model efficiency, chip partnerships, and data center arbitrage—is widening, not narrowing.

Model Wars: Capability & Pricing

LLM Stats’ model release tracker records 52 new model announcements in May 2026 alone, though only 6 represent meaningful capability advances. Frontier models (GPT-5.5, Claude 4.5, Gemini 2.0) are differentiating on cost-per-inference and domain-specific reasoning rather than raw benchmark scores. LM Council benchmarks show that reasoning performance has plateaued; the gap between GPT-5.5 and Claude 4.5 on standardized reasoning tasks is <3 percentage points, down from 8-12 points in Q4 2025.

Pricing wars are fragmenting the market. GPT-5.5 Instant’s cost is estimated at $0.02-0.04 per 1M input tokens (down 60% from GPT-4’s launch price), while Claude’s Small Business tier targets $50-200/month SME subscriptions. Open-source models (Llama 3.5, Mistral 7B) remain competitively viable for latency-insensitive workloads but are losing ground in real-time applications where hallucination cost exceeds inference cost savings. The practical implication: enterprise customers are consolidating to 1-2 vendors rather than multi-model strategies, a 180-degree reversal from 2024 playbooks.

Policy & Regulatory Fragmentation

The US regulatory environment is now three-tiered: federal enforcement (FTC + CFIUS), state mandates, and sectoral rules. VerifyWise’s May 2026 overview documents that Colorado’s AI Act, California’s complex compliance regime, and Texas’s TRAIGA framework are now active, creating three distinct compliance models. Colorado requires human override for high-risk AI decisions; California mandates algorithmic impact assessments and disclosure for >$10M annual spend; Texas emphasizes transparency but defers liability to users. The compliance cost for a national SaaS vendor is estimated at $2-5M annually, a 15-25% gross margin tax on smaller companies.

Drata’s regulatory database shows 7 additional state bills pending for 2026 (Illinois, New York, Minnesota, Ohio, Florida, Arizona, Nevada). Federal action remains deadlocked, but the FTC is aggressively enforcing existing consumer protection statutes against AI vendors making unsubstantiated claims. Three enforcement actions (names withheld) have resulted in $50-150M settlements and mandatory third-party audits. For vendors, state-level compliance is now a go-to-market requirement, not a future risk.

Talent & Labor Market Signals

AI-driven workforce disruption is real but chaotic. Forrester’s AI layoff regret study shows 55% of employers regret cutting headcount for AI, with implied rehiring at 30-50% of prior salaries, often in lower-cost geographies. Meta and Microsoft’s combined 20k job cuts in Q1 have not translated into advertised rehiring, suggesting the gap between promised automation and actual deployment is widening.

Compensation pressure is bifurcating: senior AI research positions (PhD-level, published work) are seeing 15-25% salary increases and remote-first terms. Entry-level and mid-career roles are stagnating or declining. The scarcity is not in AI practitioners but in domain experts who can translate business problems into AI workflows. A data scientist who can drive $500K+ annual value from LLM deployment is worth $200-300K salary + equity; a model trainer is not.

Research Highlights

Inference Optimization on Consumer Hardware: Recent arXiv papers document systematic optimization of real-time diffusion model inference on Apple M3 Ultra non-CUDA platforms, with 2.5-3.2x speedup over unoptimized baselines. This matters because it suggests that edge deployment of multimodal models is becoming viable, reducing dependency on cloud inference and lowering latency for latency-sensitive applications (real-time image editing, on-device reasoning).

Agent Safety Layers: AgentWall, a runtime safety framework, addresses autonomous AI agent control by sandboxing action execution and enforcing guardrails. Empirical results show 98.7% false positive rate reduction compared to naive filtering, enabling more reliable agentic deployments in regulated domains (finance, healthcare, critical infrastructure). This is a proxy for market readiness: agents are moving from proof-of-concept to production, and safety is no longer optional.

Credit Assignment in Multi-Step Reasoning: Recent work on credit assignment variance in LLM reasoning reveals that sparse terminal rewards (reward only at final step) reduce multi-step reasoning performance by 12-18% relative to step-wise rewards. Implication: fine-tuning LLMs for complex reasoning requires intermediate supervision, not just outcome labeling. This constrains the scalability of pure RL-from-human-feedback approaches and favors hybrid (supervised + RL) methods.

Investment Signal

1. Small Business SaaS + Agents: Companies targeting SMEs (10-500 employees) with pre-built agentic workflows will see 3-5x ARR growth by Q4 2026. Anthropic’s Claude for Small Business release and PwC’s enterprise deployment signal market pull. Trigger: track logos and NRR >120% at these vendors by Q3 2026.

2. Inference Infrastructure & Optimization: Companies building cost-reduction layers (quantization, distillation, edge deployment) will consolidate 60% of venture funding in the inference/opsz category by Q3 2026. Frontier models are becoming margin-limited, creating arbitrage for efficiency vendors. Trigger: watch for infrastructure startups raising Series B at >$50M valuations with <18-month payback on infrastructure investment.

3. Regulatory Compliance as Sticky Revenue: Vendors selling AI compliance, auditing, and governance tools will see 4-6x bookings growth through Q3 2026 as Colorado, California, and Texas rules take effect. Current market size is <$500M; it will exceed $2B by end of 2026. Trigger: monitor which compliance vendors land first three customers in highly regulated sectors (healthcare, financial services, public sector).

Related Analysis

Small Model + Smart Guardrails Jumps from 53% to 99% on Agent Tasks: The Efficiency Breakthrough That Makes Smaller Models CompetitiveMay 20, 2026

Small Model + Smart Guardrails Jumps from 53% to 99% on Agent Tasks: The Efficiency Breakthrough That Makes Smaller Models CompetitiveMay 20, 2026 314 npm Packages Hijacked in One Campaign. The Assumption That Got Everyone Killed.May 19, 2026

314 npm Packages Hijacked in One Campaign. The Assumption That Got Everyone Killed.May 19, 2026 Iran Bypasses Oil Sanctions With Bitcoin Insurance – and It’s Already WorkingMay 18, 2026

Iran Bypasses Oil Sanctions With Bitcoin Insurance – and It’s Already WorkingMay 18, 2026 The 45-Cent Problem: How AI Subscriptions Are Quietly Reallocating Corporate AmericaMay 17, 2026

The 45-Cent Problem: How AI Subscriptions Are Quietly Reallocating Corporate AmericaMay 17, 2026